October 14, 2019

Retail Radar – The Shadow of Christmas Past

Uncategorised

October 14, 2019

Uncategorised

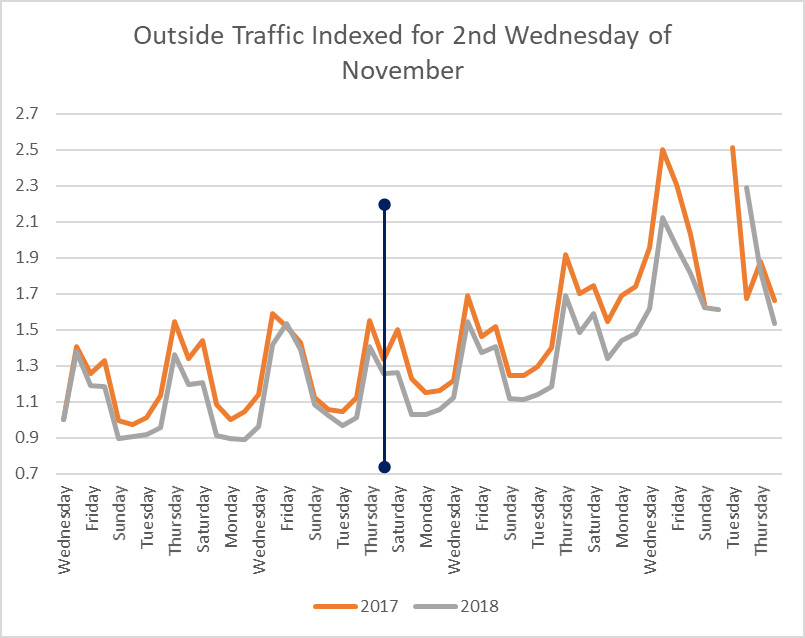

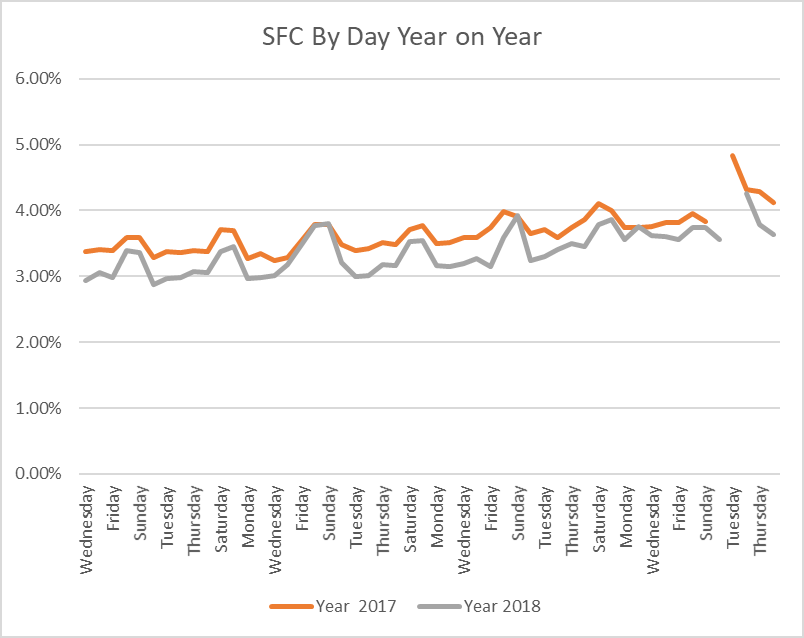

Kepler has reviewed the first five months of...

August 1, 2022

Whether we’re talking about a small chain of...

July 13, 2022

Any business owner or marketer worth their salt...

July 13, 2022

Foot traffic is one of the most important...

July 13, 2022

Simply fill in your details below and we will be in touch to arrange your free custom assessment and comprehensive demo.